ECON-1010-A-Introduction to Microeconomics

Looking for ECON-1010-A-Introduction to Microeconomics test answers and solutions? Browse our comprehensive collection of verified answers for ECON-1010-A-Introduction to Microeconomics at moodle.uleth.ca.

Get instant access to accurate answers and detailed explanations for your course questions. Our community-driven platform helps students succeed!

When a perfectly competitive firm produces the quantity at which the market price is equal to minimum average total cost, which of the following outcomes arise?

❌

❌

❌

❌

✅✨

View this question

| Table 11.2.1 |

❌

❌

✅

❌

❌

View this question

| Table 11.2.1 |

❌

0%

0%

0%

0%

View this question

| Table 11.2.4 |

0%

❌

0%

0%

0%

View this question

If market supply in a perfectly competitive market increases, which of the following events occur?

0%

50%

0%

❌

0%

View this question

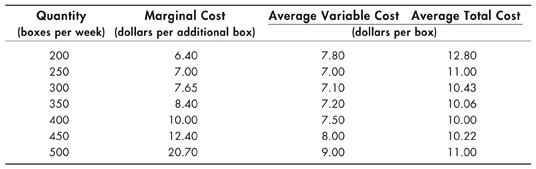

Table 11.4.1 Refer to Table 11.4.1, which shows a perfectly competitive firm's costs when it uses its least-cost plant to produce paper. If, in the short run, the market price is $8.40 per box, what changes occur in the market in the long run? In the long run, the market price ________ a box and the equilibrium quantity produced by each firm in the long run ________ boxes a week.

Refer to Table 11.4.1, which shows a perfectly competitive firm's costs when it uses its least-cost plant to produce paper. If, in the short run, the market price is $8.40 per box, what changes occur in the market in the long run? In the long run, the market price ________ a box and the equilibrium quantity produced by each firm in the long run ________ boxes a week.

0%

0%

100%

0%

0%

View this question

| Table 11.2.5 |

0%

0%

0%

0%

100%

View this question

In which of the following situations does a firm in a perfectly competitive market maximize its profit?The firm produces the quantity of output at which

✅

❌

❌

❌

❌

View this question

| Table 11.2.4 |

0%

0%

0%

0%

0%

View this question

Which of the following statements is correct?At the shutdown price in a perfectly competitive market in the short run, the market supply of the good is

❌

❌

❌

❌

✅✨

View this question

Want instant access to all verified answers on moodle.uleth.ca?

Get Unlimited Answers To Exam Questions - Install Crowdly Extension Now!